Study on email marketing in e-commerce 2023

Every year, we analyse the email marketing of the 1,000 top-selling online shops in Germany and in 2023 we continued to do this on behalf of E-commerce market study by EHI Retail Institute and the eCommerceDB did it. The results are similar to what we have already done in recent years and also in our Year-to-year comparison 2022 have found out:

Here you can find the latest analysis results for Email marketing of the top 1000 e-commerce companies in Germany 2025

ESP market shares 2023 and marketing trends: Where is the innovation?

- Email remains a “must-have” for online marketing: 89.2% of all shops examined send marketing emails, only 6.1% do not offer any newsletter subscription. *

- Almost all shops use an email service provider (ESP) or a sending service, namely 97.4% of the 892 shops from which we received at least one marketing email in the twelve-month investigation period. **

- The 20 most used platforms are exactly the same as last year, even though the order is not the same.

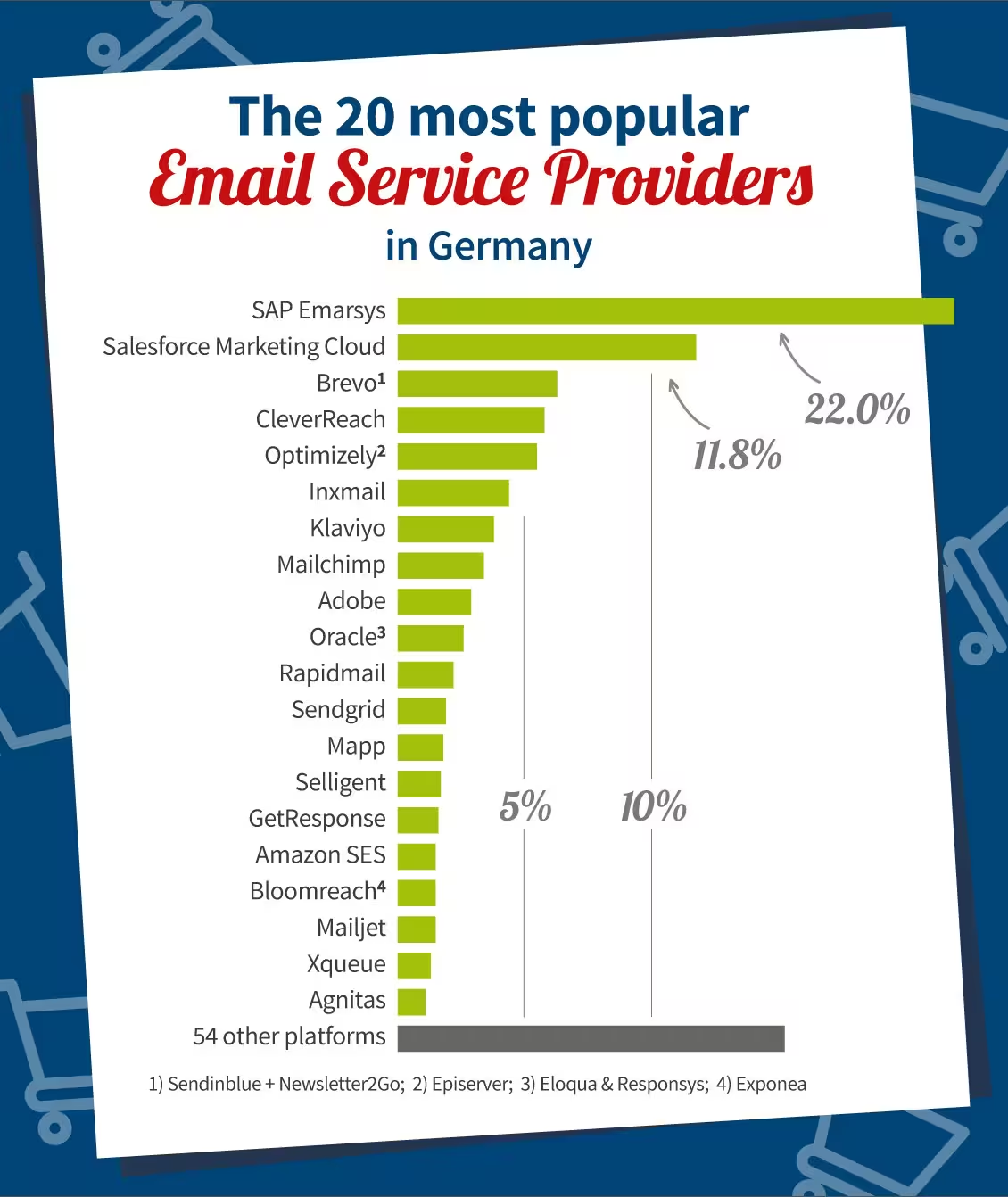

The 20 most used email delivery systems 2023

At the top is again SAP Emarsys, followed by Salesforce Marketing Cloud. The two stably cover around a third of the surveyed market, with a slight upward trend (33.8% compared to 32.3% in 2022). Optimizely, which we already diagnosed with a five-year decline in market shares in the previous year, continues to lose to just 5.5% of shops in our analysis and slips behind among the most-used platforms in e-commerce CleverReach and Brevo (the new name for Sendinblue including Newsletter2Go). These two “self-service” platform providers have switched their positions, CleverReach from 6.4 to 5.8%, Brevo from 5.4 to 6.3%. Here, too, a trend of recent years continues. Otherwise, you can still easily gain Klaviyo, Rapidmail, BloomReach and GetResponse — and in all cases, a continuation of longer-term development. Only Mailjet is winning against the trend: 1.5% after 1.3% in the previous year, but 2.0% in 2021. The remaining platforms represented maintain their share (such as Mailchimp at 3.4%) or record slight losses, including Oracle Marketing Cloud and the Sending Service Amazon SES.

Overall, we still see a highly fragmented market with a small top group of powerful multi-channel tools, which, however, have apparently exhausted their market segment to a greater or lesser extent, and a disparate midfield with a “long tail” of providers with market shares of less than 1%. Not new, but remarkable is that after the top 20 there are still 54 (!) Other platforms with a total market share of 15.3% are coming — i.e. more than the second-listed Salesforce Marketing Cloud. The 873 largest online shops in Germany with an identified sending solution therefore rely on 74 different manufacturers.

Where is the innovation?

Why does the provider landscape remain highly fragmented? Shouldn't markets with many similar products consolidate as they mature? In online business in particular, providers benefit from scale and network effects because revenue rises rapidly as the number of customers grows, but personnel and development costs do not. Although the slow but steady decline of Optimizely, for example, can be interpreted as a selective signal of concentration, if you only look at the area of “enterprise” solutions: ESPs in this segment together make up around 40% of the market, and Salesforce has been gaining more here for years. Self-service platforms such as Brevo and CleverReach (with “Made in Germany” and “Made in Europe”) are also gaining ground in the “middle segment”. However, this is not a broad-based consolidation; the forces of persistence are obviously stronger. Perhaps the ratio applies: Switching costs and involves risks. Perhaps digital marketers simply follow the motto “Never change a running system.”

But that also means that the need for new functions doesn't seem too high; the suffering from dusty or simply crude user interfaces in some of the “legacy” solutions seems bearable. In any case, no platform has apparently succeeded in inspiring marketing teams with an outstanding “must-have” feature or service — although, as is well known, the tools are constantly evolving and promise new opportunities. Whether it's AI, customer data platform, shop system integration, web push or interactive elements: There is apparently no provider who brings such paradigmatic and unique innovations to the platform that they trigger a massive market shift. The market seems mature and saturated; you could also say heresically: sluggish.

Conclusion: At some point, the Tesla of email marketing may come along and shake up the market, but not yet today. Financial and personnel considerations are currently in the foreground when using the platform. In times of increased costs and falling margins, online shops must keep their email marketing expenses flat. This is also reflected in the emails: They have to sell products. There is little room and time for complex extras, as our new content analysis shows.

What's in it: prices, products, layout and elements

For the first time this year, out of all the “Top 1,000” online shops from which we received emails during the investigation period, we also looked at at least the last four emails received and rated them qualitatively. True, this is only a snapshot. But that's exactly why it gives a good impression of the current state of email marketing in e-commerce.

The recipe for marketing success is obviously: A lot, fast and, best of all, simple. E-mails are produced at high frequency and with few “bells and whistles,” i.e. without much preface, without scenic images, without “cool” functions — and with little variance in presentation. At best, it can be an animated GIF.

Turnover instead of story

- Little copy text, lots of products: 88% of shops focus clearly on products and product sales in all newsletters and not on storytelling and context. Only 10% of shops use longer texts for background topics and product descriptions in all newsletters.

- It fits in with the fact that products are primarily shown directly and without people (77%).

- The aim is to sell — and that works best with appropriate incentives: 41% point out discounts and special promotions in the shop in all newsletters viewed and a further 38% in some of the newsletters viewed. This also applies to the E-commerce subject lines that we used in the previous year's study had investigated.

- Almost half of the shops (49%) do not mention any specific prices in their newsletters. Of the 51% of shops that quote prices in their newsletters, 41% emphasize the offer character by offering a corresponding cutoff price.

Diversity of topics instead of focus

- 64% of online shops integrate multiple topics in all newsletters and display products from different product categories.

- Only 26% of shops each have one main topic per newsletter and don't show any other products or categories in this issue.

- How are customers addressed? 45% first name, 39% simmer. The rest completely avoids direct contact.

- Integrate 20%”Trust elements“like seals and awards in their emails to highlight the trustworthiness of the online shop. Examples include Trusted Shops, EHI, TÜV, Trustpilot, Chip, ComputerBild or NTV, which are used as a guarantee of shop quality. There are also very creative people who simply create seals themselves.

Templates instead of pixel art

- Most shops use a uniform basis for their emails, such as templates, so that the newsletters of a brand are similar. This ensures a high level of recognition and fast and efficient production. 53% of newsletters look very similar from issue to issue and 30% largely similar. Only 1% of shops send very individually designed emails every time.

- The visual connection to the brand and the shop is ensured by a CI-compliant design, branding and logos.

- 73% of online shops have recreated a navigation similar to the one on the website in their emails, which links to important and popular shop categories.

- The vast majority of newsletters have white as the background color or a light base tone (67% of emails primarily white, 11% monochrome light). Only very few shops (2%) create a design with only black or a dark primary color, i.e. “dark mode first”.

Proven instead of innovation

- Every year, email marketing experts announce trends of the year in the industry media. So it is a trend more interaction options in emails to integrate, for example via gamification elements, sliders, interactive galleries, surveys or simple polls based on the principle of “Did you like this newsletter?” According to our analysis, 94% of advertisers don't do that. Only 6% want the recipient to engage in such interactions.

- It is also fitting that only 13% of shops give their recipients the opportunity to use a Interest Management or Preference Center to manage their newsletter preferences and topic preferences. Read more about this topic here.

- Another trending topic should be the integration of Customer testimonials, user-generated content, and reviews be. But only 4% of shops include customer ratings and reviews in the emails we see.

- Social media content wErden rarely uses 1:1: only 6.6% integrate YouTube videos or Instagram posts into their newsletters. However, 85% point to their social media presence through icons.

Finally, a figure that may really indicate a small trend: After all 20% of senders now do not include a link to the online version of their email advertising. When clicked, this link opens the personalized email as an HTML page in the web browser. The importance of the online version link appears to be declining. Technically, there aren't many reasons why you need it anymore. But many people don't want to say goodbye completely: Many emails now “hide” the link to the online version in the footer — even though it loses its original meaning as a quickly accessible way out of “unreadable” emails.

The market shares of 74 email service providers among the EHI top 1,000 e-commerce companies in Germany

Here is a 6-year comparison of which email marketing delivery solutions are used and how often by the e-commerce companies examined:

Other email service providers

About the methodology

Basis: Evaluation of the 1,000 best-selling B2C online shops and the top 10 B2C marketplaces in 2023, determined by EHI Retail Institute and eCommerceDB:”Study: E-Commerce Market Germany 2023", sorted by e-commerce sales in fiscal year 2022.

* Online stores that sent at least one marketing email in the 12-month investigation period in percent. n = 892.

** Online shops that sent emails via a sending platform identified as an ESP, shop module or sending service* during the 12-month investigation period. The percentage market share is calculated from the number of companies for which the respective sender was identifiable. n = 873.

*** excluding companies that use this sending service as backend senders of marketing automation — in this case, the “front-end” tool was included in this list (if the respective ESP was identifiable).

**** Sending services are ranked for the first time in 2021