Why do the 1000 largest online shops use 66 different email marketing platforms?

As part of the study “E-Commerce Market Germany 2019", we investigated whether and How Germany's thousands of largest online shops do email marketing. Although email marketing is a technology that has been established for years, there is no consolidated market and little change in the tools used. Although we were able to identify 66 different email service providers, there are a few top dogs among them: The ten most-used platforms serve 76% of the online shops surveyed, the 20 most common even 88%. In 2019, there were eleven new entrants compared to the previous year's study, which cover 2.3% of the examined email service provider market segment.

When is a market a market?

Based on the results, we can not only read the market shares of email marketing platforms, but also make statements about the market itself.

Already with a Investigation of email marketing at around 3700 shops in the USA, which we conducted in 2016, there was a discussion among experts as to whether you can lump together powerful multichannel platforms with lean email self-service platforms or whether apples are compared with oranges here. So are we talking about several markets that are not in competition with each other?

To understand this, we have sorted the 66 platforms from 2019 by breadth and depth of functionality, focus areas, integrated channels, and availability of personal account management and professional services. We were able to divide providers into four main groups:

- multichannel marketing: e.g. Emarsys, Episerver (Optivo), Mapp, and Cheetah Digital

- Multi-channel multi-cloud: such as Salesforce Marketing Cloud, Adobe Marketing Cloud, Oracle Marketing Cloud, and SAP Marketing Cloud

- Regional and email focus: e.g. Inxmail, Xqueue, Agnitas and Mailingwork

- Self-service email marketing: e.g. CleverReach, Mailchimp, Sendinblue (Newsletter2Go) and Rapidmail

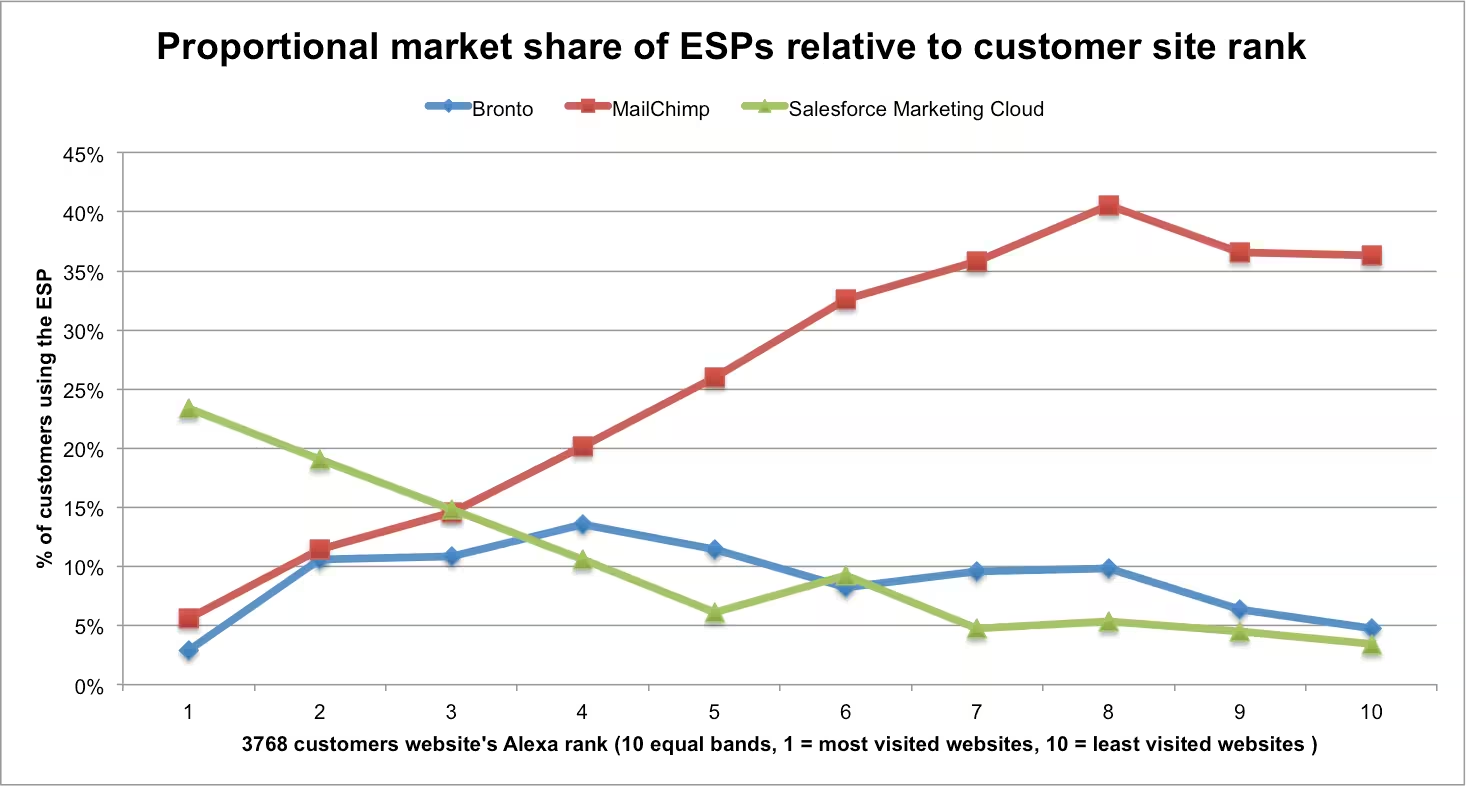

All groups are represented among the five most frequently used solutions. We divided the entirety of online shops into five equal groups (quintiles) according to their EHI rank and then compared how often the most used solution from each of the four main email marketing groups is used.

Although emarsys is most commonly used by top-selling shops, this difference is quickly flattening out. The other solutions are even represented relatively consistently. Even though CleverReach is little represented as a self-service platform in the first quintile, but almost comes close to emarsys in the last quintile: All solutions are represented in all groups. There can be no question of separate markets. This is in line with the results of our above-mentioned US study.

The result is the same despite different methods. Although we looked at a different country, a different population and a different definition of size, no clear distinction is possible here either; despite a discernible correlation between company size and tools. The largest companies certainly use large enterprise solutions, but they also use supposedly simple tools for their email marketing — or specifically: 6% of the “biggest tenth” (decile) used Mailchimp. But why is that the case?

Maximizing benefits versus minimizing costs

Which platform is the right one?

When choosing a platform, companies pursue two different strategies: maximizing benefits versus minimizing costs.

The benefit maximizers want to get the most out of every customer — i.e. optimize customer lifetime value. To do this, they tend to need a comprehensive multi-channel solution with cross-channel journey orchestration. Accordingly, they are prepared to invest in technology, advice and service.

Cost minimizers, on the other hand, want “straightforward” and functional email marketing. They send successful marketing emails, but rather avoid complex technical integrations, complex automation and cross-channel prospect tracking.

Both strategies can be found in every segment and are ultimately aimed at the highest possible margin. One criterion can be potential customer value: For a furniture shop, the sales potential that can be activated is probably higher than for a specialized contact lens shop. The question of “strategy fit” when selecting tools is therefore much more important than individual features or even costs.

In individual cases, these strategies will not be formulated as here. However, they explain why there is a fragmented market, but it is only one market. We will continue to watch where the trend is heading!